Are the Magnificent 7 Overvalued?

Sky-high price-to-earnings ratios and a higher for longer interest rate environment due to sticky inflation have left many investors skeptical regarding the valuations of the Magnificent 7. The Magnificent 7 currently boast an average trailing P/E of 42.11 and an average forward P/E of 36.84, signaling to many fundamental analysts that the stocks are too expensive. CPI releases continue to disappoint, leaving the Fed intent on holding interest rates above 5% and casting doubts over the future performance of the largest companies in the US. However, according to the Bloomberg Magnificent 7 Total Return Index, the group has returned 22% since the beginning of 2024, disregarding those preaching overvaluation.

For an established group such as the Magnificent 7, ratios are just a piece of the valuation puzzle. Firstly, the companies within the 7 (Apple, Microsoft, Google, Amazon, Meta, Nvidia, and Tesla) have maintained high growth estimates and are dominant players in their respective markets. Strong competitive positioning and deep integration into our society give each company a good chance at outlasting and rebounding after a potential market catastrophe. In addition, passively buying the S&P 500 is an increasingly popular strategy for savers. This trend shows no signs of stopping, indicating that indiscriminate passive inflows will continue to inflate the prices of the Magnificent 7. The Magnificent 7 hold benefits that other companies do not, and many of these benefits cannot be valued with something as simple as a price-to-earnings ratio. The high growth estimates, market dominance, deep integration, and indiscriminate passive investments give the Magnificent 7 lower perceived risk and higher inflows than their smaller counterparts. This is what makes the Magnificent 7 stocks perfect contenders for valuation with the capital asset pricing model (CAPM), which provides valuations using required rates of return based on risk.

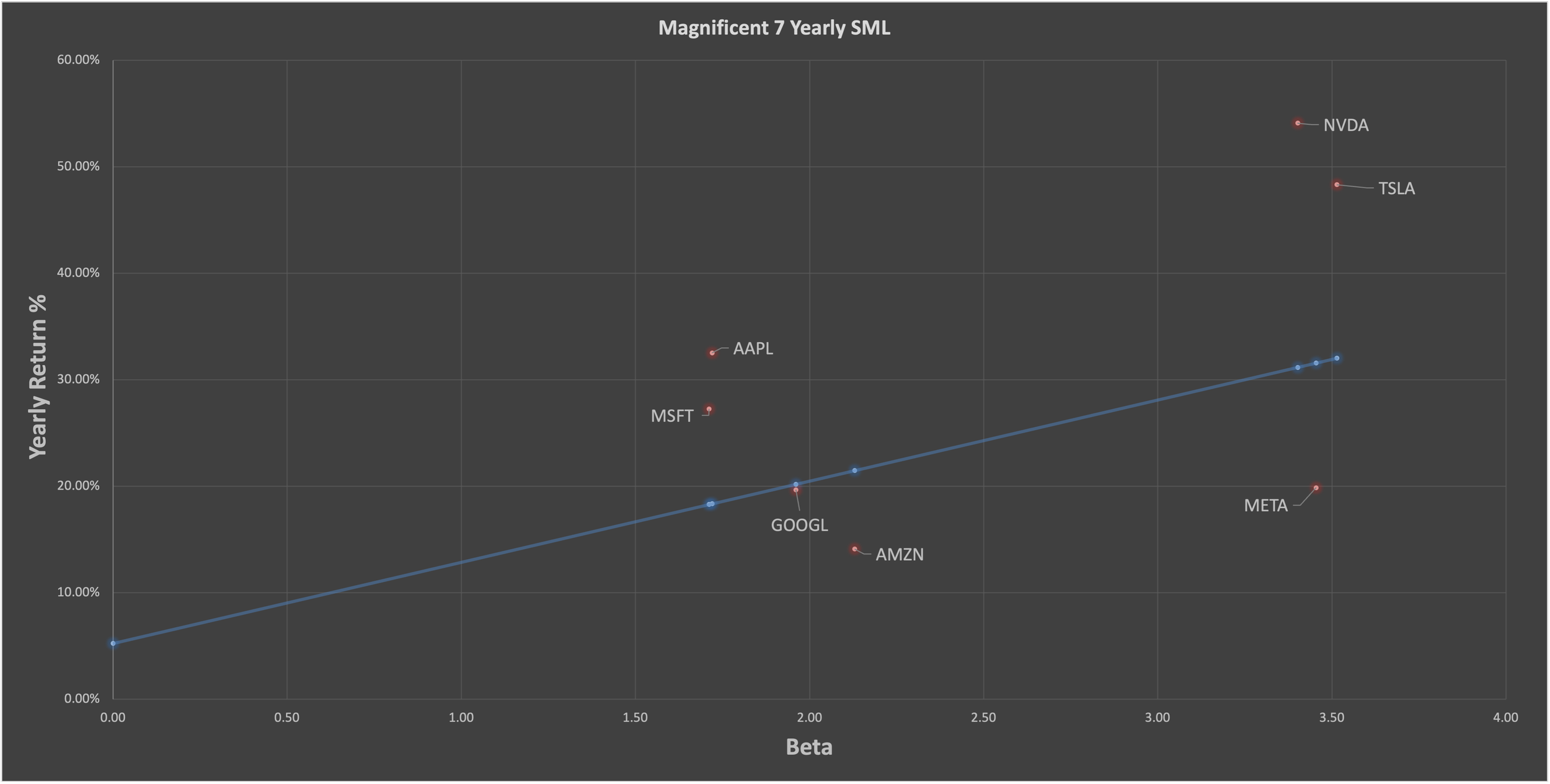

The required rate of return for each stock falls along the security market line (SML) and is calculated using the risk-free rate, the stock’s sensitivity to the market (beta), and the market risk premium, which is the expected return of the market in excess of the risk-free rate. These required rates of return are compared with expected rates of return to determine whether a company is likely to make excess returns and is thus undervalued or if it is expected to underperform, leaving it to be overvalued. The pricing data comes from the past five years to best incorporate the current business cycle and calculate a reliable beta, while the current annualized 13-week T-Bill rate is used as the risk-free rate.

Using the geometric average of annual returns for the past five full years (beginning of 2019 to the end of 2023) as an estimate for future expected returns, Nvidia, Tesla, Apple, and Microsoft are expected to return more this year than required based on their risk, making them undervalued. Google, Amazon, and Meta are expected to return less than required, making them overvalued.

Magnificent 7 Annualized CAPM Analysis

Five months into 2024, the forecasted undervalued companies have won against the S&P on an equally weighted portfolio basis. Microsoft yielded a 12% return, Nvidia yielded 86%, Tesla dropped nearly 30%, and Apple stayed more or less stagnant with a year-to-date return of around -1%. These results align with calculated expected returns, with the exception of Apple and Tesla. Apple suffered a drop mainly due to a DOJ lawsuit regarding monopolization but has since recovered. Tesla faced a slurry of issues this year, including a threat to their market dominance from the Chinese EV company BYD. This is an excellent example of how returns from the Magnificent 7 can have more to do with perceptions than their prices being too high for their earnings. While Tesla and Apple fell during risks to their perceived dominance, forward P/E ratios for Microsoft and Nvidia currently sit at 31.45 and 38.14, respectively. Regardless of Tesla and Apple’s early drop, an equally weighted portfolio of the forecasted undervalued stocks within the Magnificent 7 would have yielded approximately 16.75% since the start of 2024, beating the S&P500’s return of 11.18%.

Aside from pure valuation, the CAPM model allows one to dive deeper into the relationship between returns and risk. The further to the right a stock is on the security market line, the higher its sensitivity to the market, measured by beta. The chart above shows that Nvidia and Tesla have the largest expected excess returns, but they also have relatively high betas, meaning that a downturn in the market will likely cause more pain to their investors than those in Apple or Microsoft. This is important to account for when making investment decisions based on CAPM analysis.

Another critical point to note is that the standard deviations of annual returns for the stocks within the Magnificent 7 are much higher than that of the S&P in the last five years, which was 20%. In contrast, Tesla's five-year standard deviation of annual returns is around 326%. Taking statistical risk measures into account, such as beta and standard deviation of returns, is well worth the effort when picking investments.

Annualized betas are higher than traditional monthly betas, and the standard deviations of yearly returns are far more significant than those of monthly returns. Considering that many active investors have expected holding periods of less than a year, it would be amiss not to analyze the Magnificent 7 on a monthly basis.

Magnificent 7 Monthly CAPM Analysis

The monthly CAPM security market line, which uses monthly logarithmic return data from the start of 2019 to the end of last month, labels all 7 stocks as undervalued. Monthly nominal returns for all 7 stocks have averaged between 1% and 6% during the past 5 and half years, compared to the S&P’s 1%. The 5-year monthly betas for all 7 stocks are between 0.5 and 2.3, making them far less risky than their annualized counterparts, which are between 1.5 and 3.6. When adjusting for their lower relative systematic risk on a monthly basis, all 7 stocks will likely produce excess returns, making each a solid choice for investors with monthly holding periods. In addition, their monthly standard deviations of returns, used as a measure of total risk, all fall below 20%, with the exception of Tesla at 22%.

While the capital asset pricing model is a great tool for valuation, it is by no means perfect. Expected returns are often reasonable estimates but are never an exact science. The most important takeaway is understanding what return should be required from a stock when considering its riskiness over the investment holding period. In the case of the Magnificent 7, the CAPM method helps provide reasoning for the continued growth of stocks whose traditional financial metrics may suggest they are overvalued. It is always necessary for investors to consider as many factors as possible, and the CAPM model is just one of many pieces that make up the puzzle of security analysis.